Private equity is widely recognized for its potential to generate attractive long-term returns. However, investors entering the asset class often encounter a phenomenon that can be surprising at first: negative returns during the early years of a fund’s life.

This pattern is commonly known as the J-Curve in private equity, a structural feature of the asset class that reflects how value is created over time.

Understanding the J-Curve is essential for investors allocating capital to private markets, as it directly affects performance expectations, liquidity planning, and portfolio construction.

What Is the J-Curve in Private Equity?

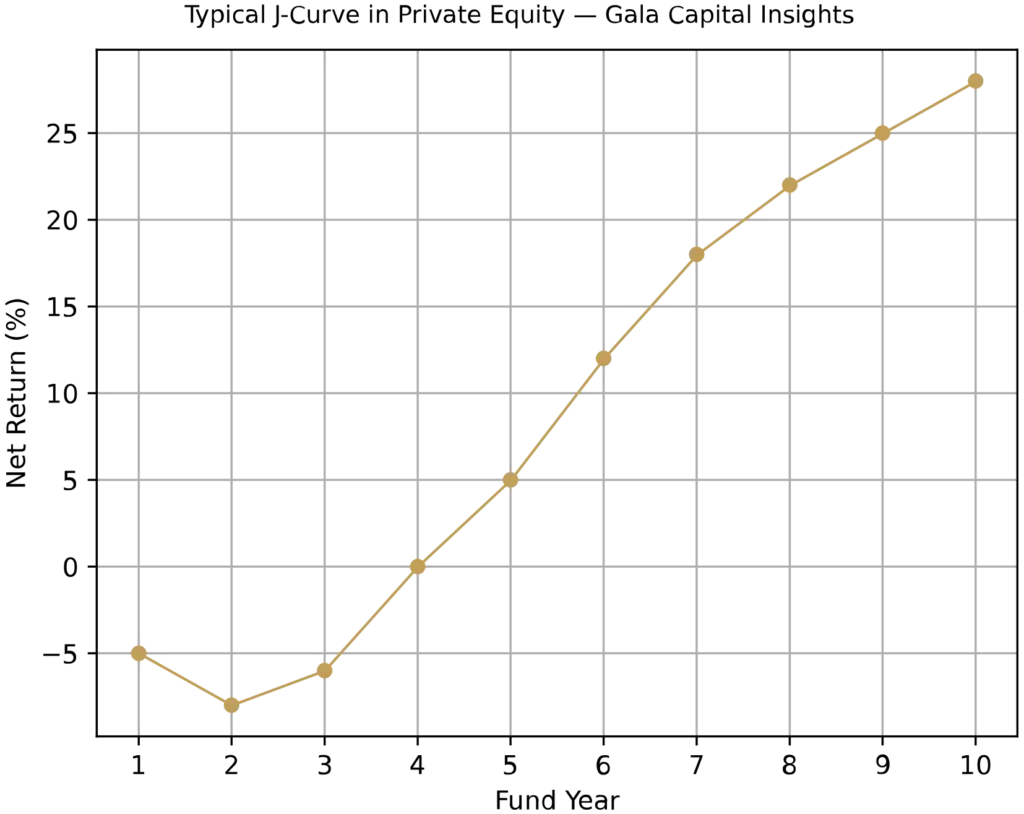

The J-Curve describes the typical evolution of returns in a private equity fund throughout its lifecycle.

In most cases, a fund’s performance follows three stages:

- Initial decline in value during the first years

- Gradual recovery as portfolio companies develop

- Strong positive returns when investments are exited

When plotted over time, this pattern resembles the shape of the letter “J”—returns dip early before rising significantly later.

This dynamic is a well-known characteristic of private equity, venture capital, and other private market strategies.

Why the J-Curve Happens

Several structural factors explain why private equity funds experience negative returns in the early years.

Management Fees and Initial Costs

Private equity funds typically charge management fees from the beginning of the investment period.

These fees, along with transaction costs and organizational expenses, reduce early reported returns before portfolio companies begin generating value.

As a result, investors may initially see negative net performance, even though the underlying investments may still be in their early development phase.

Time Required to Create Value

Private equity investments are designed to generate value through active ownership and long-term strategic improvements.

Portfolio companies often undergo:

- operational restructuring

- management optimization

- growth initiatives

- strategic acquisitions

- market expansion

These transformations take time, meaning that value creation usually materializes several years after the initial investment.

Conservative Valuations in Early Years

Another reason for the J-Curve is the conservative valuation approach used in private markets.

Until a liquidity event occurs—such as a sale, recapitalization, or IPO—portfolio companies are typically valued cautiously. This means that significant value increases may only appear later in the fund’s lifecycle.

When exits occur, these realized gains can substantially increase the fund’s performance, driving the upward part of the J-Curve.

A Typical Private Equity Fund Lifecycle

Most private equity funds operate with a 10-year structure, generally divided into two phases.

Investment period (years 1–5)

During this stage, the fund deploys capital into portfolio companies. Returns often remain negative due to fees, initial costs, and unrealized value creation.

Harvesting period (years 5–10)

As portfolio companies mature, the fund begins to exit investments. These exits generate distributions to investors, often producing the strongest returns.

This transition from early investment to later realization is what drives the upward movement of the J-Curve.

Implications for Investors

For investors allocating capital to private equity, the J-Curve has several important implications.

Long-Term Investment Horizon

Private equity is inherently a long-duration asset class. Investors should expect meaningful returns to emerge later in the fund lifecycle rather than in the initial years.

Patience and a clear long-term strategy are therefore essential.

Liquidity Planning

Private equity funds use a capital call structure, meaning capital is drawn over time rather than invested all at once.

At the same time, distributions typically occur later in the fund’s life. Investors must therefore manage liquidity carefully to meet capital calls while waiting for returns.

Vintage Year Diversification

Institutional investors often mitigate the J-Curve effect by investing across multiple fund vintages.

By allocating to funds launched in different years, investors create a portfolio where:

- some funds are still investing

- others are already generating distributions

This approach helps stabilize overall cash flows and reduces the impact of early negative returns.

Strategies to Reduce the J-Curve Effect

While the J-Curve is inherent to private equity, several strategies can help moderate its impact.

Secondary investments

Purchasing interests in more mature private equity funds allows investors to access portfolios that are closer to the realization phase.

Co-investments

Investing directly alongside private equity managers often reduces fee structures and accelerates exposure to underlying assets.

Diversified private market portfolios

Combining different strategies—such as buyouts, growth equity, and secondaries—can create a more balanced return profile over time.

Final Thoughts

The J-Curve in private equity is not a flaw of the asset class but rather a reflection of how value is built through long-term investment strategies.

Early negative returns are typically followed by stronger performance as portfolio companies mature and successful exits occur.

For investors who understand this dynamic and plan accordingly, private equity can play a powerful role in diversifying portfolios and generating long-term value.