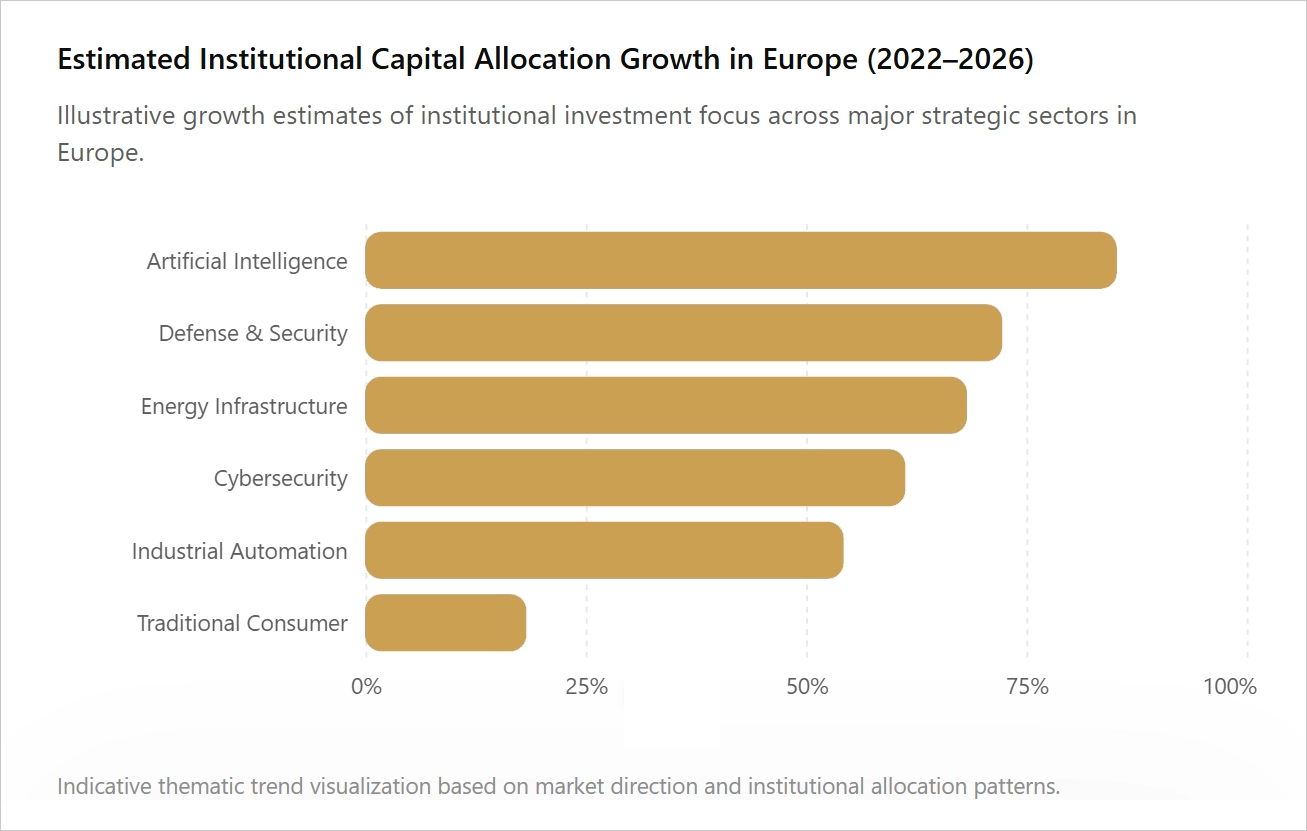

Why Institutional Capital Is Repositioning Across Europe

European capital markets are undergoing a structural transformation. After more than a decade dominated by low interest rates, globalization, and digital consumer growth, institutional investors are now reallocating capital toward sectors directly linked to sovereignty, resilience, and strategic autonomy.

Three themes increasingly dominate investment committees across Europe:

- Artificial Intelligence (AI)

- Defense and security

- Energy transition and energy independence

These are no longer niche allocations or speculative trends. They have become central pillars of European industrial policy, private equity deployment, infrastructure investment, and long-term institutional asset allocation.

For investors, understanding these themes is no longer optional. They are shaping valuation multiples, M&A activity, fundraising dynamics, and the future direction of European investment flows.

The New Macro Regime Behind European Investment Trends

The current investment environment is fundamentally different from the one that defined the 2010s.

Several structural forces are reshaping European markets simultaneously:

- Persistent geopolitical fragmentation

- Reindustrialization across Europe

- Higher structural inflation

- Supply chain security concerns

- Increased fiscal intervention

- Technological competition with the United States and China

- Energy dependency risks exposed by the Ukraine conflict

As a result, governments and institutional investors are prioritizing strategic sectors capable of strengthening European competitiveness and resilience.

This shift explains why AI, defense, and energy have become the defining investment themes in European capital markets.

Artificial Intelligence: Europe’s Race for Technological Sovereignty

Artificial Intelligence is no longer viewed solely as a software trend. It is increasingly treated as strategic infrastructure.

European policymakers recognize that AI leadership will influence:

- Productivity growth

- Industrial competitiveness

- Cybersecurity

- Defense capabilities

- Financial services efficiency

- Healthcare innovation

While the United States currently dominates large-scale AI infrastructure and frontier models, Europe is accelerating efforts to build its own ecosystem through:

- public-private partnerships,

- semiconductor investments,

- cloud infrastructure,

- sovereign AI initiatives,

- and industrial automation programs.

Where Capital Is Flowing

Institutional investors are particularly focused on:

AI Infrastructure

Data centers, GPUs, cloud architecture, and digital infrastructure platforms are attracting significant private capital.

Industrial AI

Europe’s manufacturing base creates strong opportunities for AI-driven automation in logistics, industrial software, robotics, and predictive maintenance.

Cybersecurity

As digitalization expands, cybersecurity has become one of the fastest-growing investment verticals across Europe.

Vertical AI Applications

Healthcare, legal services, financial services, and industrial engineering are seeing rapid adoption of specialized AI solutions.

Why Private Equity Is Interested

Private equity firms view AI not only as a growth sector, but also as a value creation lever across portfolio companies.

Operational AI integration can improve:

- EBITDA margins,

- pricing optimization,

- customer acquisition efficiency,

- and supply chain management.

In many cases, the most attractive investments are not necessarily AI model developers, but rather the infrastructure and enterprise software businesses enabling adoption at scale.

Defense: From Political Constraint to Strategic Priority

For decades, defense was largely underweighted in European institutional portfolios due to political sensitivities and ESG constraints.

That paradigm has changed dramatically.

Russia’s invasion of Ukraine fundamentally altered Europe’s perception of security and defense spending. NATO members across Europe have committed to significantly increasing military budgets, while the European Union is actively supporting defense industrial expansion.

Defense is now increasingly viewed as:

- a strategic necessity,

- an industrial policy priority,

- and a long-term investment theme.

The Scale of the Opportunity

European governments are allocating hundreds of billions of euros toward:

- military modernization,

- cybersecurity,

- aerospace systems,

- ammunition production,

- satellite infrastructure,

- and defense technology.

This creates substantial opportunities across both public and private markets.

The Rise of Defense Tech

One of the most important developments is the emergence of defense technology as a venture and growth equity category.

Investors are increasingly backing companies involved in:

- autonomous systems,

- AI-powered defense applications,

- drone technologies,

- cybersecurity,

- advanced sensing systems,

- and space-based intelligence platforms.

This convergence between AI and defense is becoming one of the most strategically important areas in European innovation.

ESG Reassessment

Interestingly, institutional attitudes toward defense investing are evolving.

Many investors now differentiate between:

- offensive weapon exposure,

- and investments supporting democratic security infrastructure.

As a result, several institutional frameworks have become more flexible regarding defense-related investments, particularly in cybersecurity and dual-use technologies.

Energy: Europe’s Long-Term Strategic Imperative

Energy remains one of the most significant investment priorities in Europe.

The energy crisis triggered by the Russia-Ukraine conflict exposed the vulnerability of Europe’s historical energy model and accelerated the push toward energy independence.

Today, Europe’s energy strategy revolves around three objectives:

- decarbonization,

- security of supply,

- and affordability.

Achieving all three simultaneously requires enormous capital investment.

The Scale of Capital Deployment

The European energy transition requires trillions of euros in investment over the coming decades across:

- renewable generation,

- transmission infrastructure,

- battery storage,

- hydrogen ecosystems,

- electrification,

- and grid modernization.

This has created one of the largest infrastructure investment opportunities globally.

Why Institutional Investors Favor Energy Assets

Energy infrastructure offers several characteristics attractive to long-term investors:

- inflation protection,

- stable cash flows,

- regulated revenue frameworks,

- and long-duration asset profiles.

Pension funds, sovereign wealth funds, infrastructure funds, and private equity firms are all increasing exposure to energy-related assets.

Beyond Renewables

While renewables remain central, investors are also focusing on:

- LNG infrastructure,

- nuclear modernization,

- battery technologies,

- carbon capture,

- and energy efficiency platforms.

The investment landscape is becoming broader and more technologically sophisticated than the first generation of ESG-driven renewable investing.

The Convergence of AI, Defense, and Energy

One of the defining characteristics of current European investment trends is the growing overlap between these three themes.

They are no longer independent sectors.

Instead, they increasingly reinforce one another.

Examples include:

- AI-powered defense systems,

- energy-intensive AI infrastructure,

- cybersecurity for critical energy grids,

- semiconductor sovereignty initiatives,

- and advanced industrial automation.

This convergence is reshaping:

- European industrial policy,

- cross-border M&A activity,

- private market fundraising,

- and institutional portfolio construction.

Investors capable of understanding these interconnections are likely to identify some of the most compelling long-term opportunities in European capital markets.

Implications for Private Equity and Institutional Investors

For private equity firms, the new environment favors:

- operational expertise,

- sector specialization,

- infrastructure capabilities,

- and long-term thematic investing.

Traditional financial engineering alone is becoming less sufficient in a higher-rate environment.

Value creation increasingly depends on:

- technological integration,

- industrial positioning,

- and strategic relevance.

Meanwhile, institutional LPs are reassessing portfolio exposure toward sectors aligned with:

- national resilience,

- industrial competitiveness,

- and structural growth.

This shift is likely to remain a defining feature of European markets for the next decade.

Final Thoughts

Artificial Intelligence, defense, and energy are not temporary market narratives. They represent a structural reordering of European capital allocation priorities.

Driven by geopolitical realities, industrial policy, and technological transformation, these sectors are becoming central to how Europe defines competitiveness and economic security.

For investors, the key challenge is no longer identifying whether these themes matter.

It is understanding where sustainable value creation will emerge within them.

The next generation of European market leaders will likely be built at the intersection of technology, infrastructure, and strategic autonomy — precisely where AI, defense, and energy converge.